La confiance…

Comments are closed.

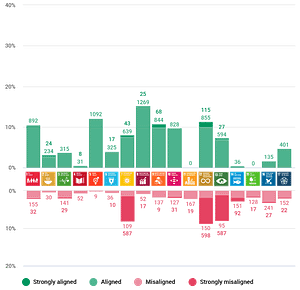

Pour illustrer cette préoccupation, rien qu’en France, nous avons les 17 objectifs verts et de développement durable hérités des Nations Unies, auxquels s’ajoutent une dizaine de labels nationaux (GreenFin, CEE, etc.). Le marché lui-même est déroutant pour le financier de bonne foi en raison du manque de cohérence entre les différentes certifications vertes. Chaque pays, en fonction de ses objectifs et de ses choix stratégiques, définit ses propres labels :

Les émetteurs de titres qui ont l’ambition d’attirer des contreparties internationales doivent choisir un camp et un label. Les investisseurs, qui sont principalement des fonds transnationaux, incluent alors dans leurs portefeuilles verts des actifs qui répondent à des exigences diverses, voire incompatibles, et, avec beaucoup d’hypocrisie, vont peupler des fonds qui répondent à la seule dénomination verte. C’est encore une fois la confiance, principal moteur du marché, qui est mise en danger par cet amalgame.

On se souvient de l’origine de la crise de 2008, qui était la titrisation et le regroupement dans des fonds d’actifs aux profils de risque incompatibles : les subprimes en l’occurrence.

#greenclaim #insurance #tracking #impact

| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |